Protection your family can count on

Offered through employers, unions, and associations, the Family Protection

Plan coverage provides financial protection with a level premium to age 121, so your payment will not change.

You can get coverage for your spouse even if you don’t elect coverage on yourself. And you can cover your financially dependent children, too.

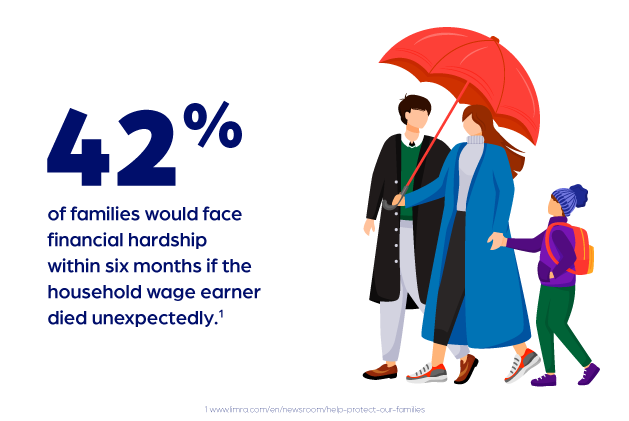

Are you prepared for the unexpected?

The journey of life can be unpredictable causing families to reassess the need for additional financial protection to keep their future secure.

Coverage benefits

Customizable

With several options to choose from, select the coverage that best meets the needs of your family.

Ease of payment

Convenient payments through your employer using payroll deduction.

Keep the coverage

As long as premiums are paid, coverage continues with no loss of benefits or increase in cost if you terminate employment after the first premium is paid. We bill you directly.

Acceleration of benefits

Pays 30% (25% in CT and MI) of the coverage amount in a lump sum upon the occurrence of a terminal condition that will result in a limited life.*

Family coverage

You can get coverage for your spouse even if you don’t elect coverage on yourself. And you can cover your financially dependent children.**

Emergency death benefit

Within one business day of notification, payment of 50% of coverage or $10,000 whichever is less is mailed to the beneficiary.***

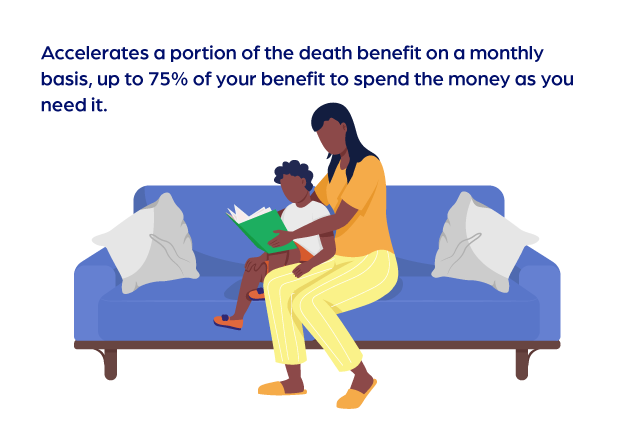

Quality of Life rider

Optional benefit payable directly to you on a tax favored basis for the following:

- Permanent inability to perform at least two of the six Activities of Daily Living (ADLs) without substantial assistance; or

- Permanent severe cognitive impairment, such as dementia, Alzheimer’s disease and other forms of senility, requiring substantial supervision.

Commonly Asked Questions About Life Insurance

What is the difference between term life and whole life insurance?

Term life insurance provides coverage for a set number of years and pays a benefit only if you pass away during that period. Whole life insurance, on the other hand, provides coverage for your entire lifetime as long a premiums are paid and builds cash value you can access over time.

What type of coverage is the Family Protection Plan?

The Family Protection Plan is group level term coverage purchased through your employer.

Will my payments change?

No. This product has a level premium to age 121, so your payment will not change.

Is coverage portable if I leave my company?

As long as premiums are paid, coverage continues with no loss of benefits or increase in cost if you terminate employment after the first premium is paid. You’ll simply receive the bill directly.

What is the Quality of Life Rider?

This optional benefit accelerates a portion of the death benefit on a monthly basis, up to 75% of your benefit, and is payable directly to you on a *tax-favored basis if you become permanently unable to perform two or more activities of daily living (ADLs) or if you develop a severe, permanent cognitive impairment.

* Accelerated benefits may, or may not, be taxable. If so, you or your beneficiary may incur a tax obligation. As with all tax matters, you should consult your personal tax advisor to assess any potential impacts of this benefit.

We're here to help

Visit the Support Center to file a claim, make a payment or change to your account, answer questions about your coverage, and more.

*Span of less than 12 months (24 months in IL), **Children (14 days to 19 years old, 26 if full-time student) under your coverage or your spouse’s, ***Unless the death is within the two-year contestability period and/or under investigation.

Product underwritten by 5Star Life Insurance Company (a Lincoln, Nebraska company). Product not available in all states. Policy #: CC18-GFPPPOL, ICC19-FPPi